It is no secret that there is a national shortage of homes for sale on the market, and with a few exceptions, that dearth of inventory is especially acute in the metro Washington, DC* area.

This has been coming for a long time. The average inventory at the end of February over the decade from 2005 – 2015 was right at 10,000 homes. At the end of February 2019 – just before the onset of the COVID pandemic – there were 7,600 available homes, and at the end of February 2024, there were less than 4,000. When you realize that the population of our area has grown 39% (1.5 million people) since 2000, that’s a staggering drop. Put simply, there’s 60% less inventory today with 40% more people.

But why is this happening? There are lots of reasons, and most are long-lasting.

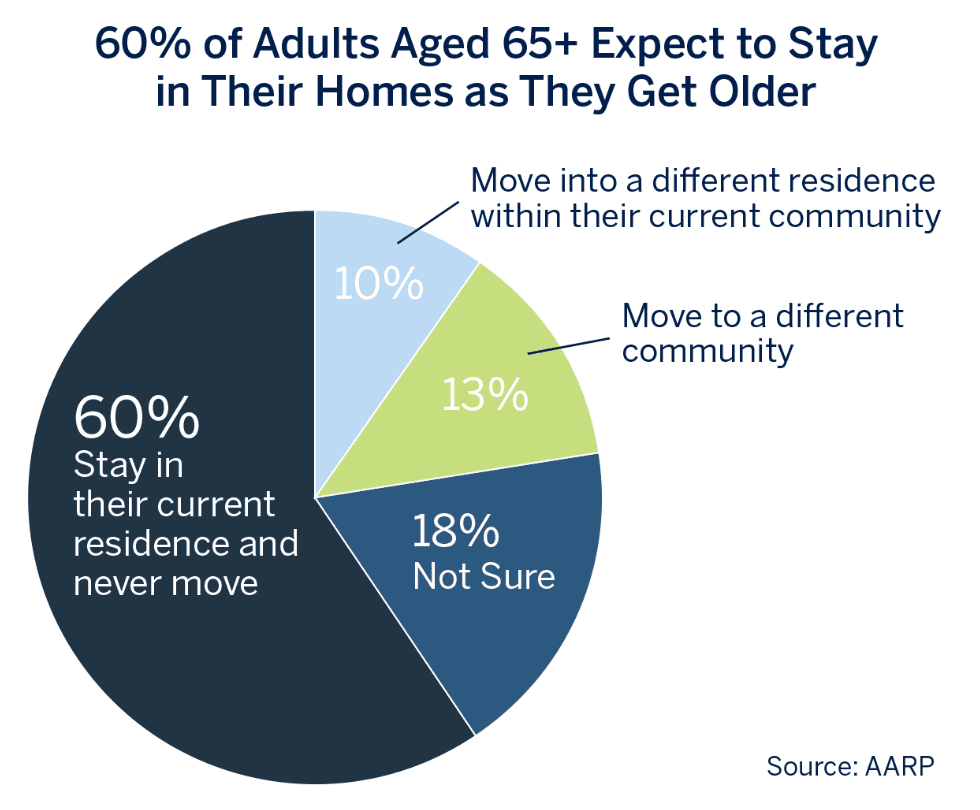

People are staying in their homes much longer. The National Association of Realtors tracks “seller tenure,” the median length of time a seller has been in their home before they sell. For a generation that stayed steady at 7 years – and it’s now more than 12. And while the Silver Tsunami, the big jump in population of aging Baby Boomers is real, the impact thus far on real estate has been a ripple at best. A recent study by AARP indicates that 60% of adults aged 65 or older have no plans to move from their current home – ever. That’s a lot of inventory that isn’t going to come on the market anytime soon.

We’ve never seen a time of such rapid increases in mortgage interest rates following record- low rates. Roughly half of all homeowners have a current mortgage at a rate of 4% or less – and many have a sub-3% mortgage. Consider this basic example: a homeowner with a $500,000 mortgage at 3% has a monthly principal and interest payment of $2,108.02. If that same homeowner sells and buys something with a mortgage that is just 10% more – $550,000 – their new monthly payment at the current rate of 7% would be $3,659.16. That’s a 74% increase in the payment for just a 10% bigger loan, and many sellers understandably won’t make that switch. On top of that, those sellers – like aging Baby Boomers – who have owned their home for a long time might face a tax hit if their capital gain exceeds $500,000. All of that has locked a lot of would-be inventory off the market.

High Cost of Land – and the High Cost of RegulationOur region has battled this for a long time, and it really restricts affordable new home construction. As intensely developed as the close-in areas of metro DC are, much of the new construction is in the outlying suburbs, and that may not be where people want to live. There have been studies that indicate as much as 25% of the cost of new construction is involved with planning and compliance with federal, local, and state regulations. That contributes to driving home prices higher, another hill to climb for current homeowners who might consider moving.

There’s Inventory – and There’s Inventory That People May Not WantThere isn’t enough inventory – except for condos and co-ops in Washington, DC. It’s another indication that there isn’t just one real estate market, and buyers really do care about what they buy even when they don’t have many choices. Through most of the last 20 years, the inventory of condos and co-ops on the market in DC constituted about 7% of all available homes. Now, it’s 25%. Much of that inventory is in older buildings with few amenities, and that’s not what today’s buyers are typically looking for. Time isn’t going to make those units better. So even in a time of scarce inventory, market dynamics still matter, and a buyers’ market can exist when almost everything else tilts in favor of sellers. Those condos and co-ops will still sell, but they will be on the market longer and won’t command the higher prices that other property types do.

What Happens From Here?Markets adjust over time. There is pent-up demand from people who would really like to sell their home, and we will see the typical increase in inventory this spring. But that rebound will be muted until interest rates come down substantially, and that’s going to take a while. And the demographic pressures really aren’t going to change. Be prepared for an extended time of inventory that is insufficient to meet the demand – and that means continuing higher home prices.

We also hear theories that the upcoming elections will have a major impact on the region’s housing – watch for our next MarketWatch where we will dispel that myth.

*Data derived from BrightMLS for Northern Virginia (Fairfax and Arlington Counties and Alexandria, Fairfax and Falls Church Cities), Loudoun County, Prince William County (including Manassas City and Park), Washington, DC, Montgomery County and Prince George’s County.